Alibaba - back of the envelope valuation

Keep it simple!

Overview

The primary reason I’m writing this is that I recently saw an article projecting Alibaba’s free cash flow for the next 10 years, predicting a market value of 600 billion US dollars or even a trillion US dollars. You really can’t make that up.

Alibaba BABA 0.00%↑ is a well-researched and followed stock, making it challenging to have a unique analytical edge. The primary opportunities for gains lie in having a different time horizon or a different perspective.

The current situation for Alibaba is straightforward, I wrote in more details here and also here.

Let me summarize the main points:

Past Management Issues

Alibaba’s previous management team was very poor, and each business segment lost to its respective competitors.

• China E-commerce: Lost market share to Pinduoduo.

• Food Delivery: Lost to Meituan.

• International E-commerce in Southeast Asia: Lazada lost its dominant position to Sea Limited.

Acquisition Problems

Daniel Zhang, the former CEO, acquired numerous underperforming assets. His strategy of merging online and offline retail through “new retail” backfired due to its asset-heavy nature, negatively impacting Alibaba’s overall performance.

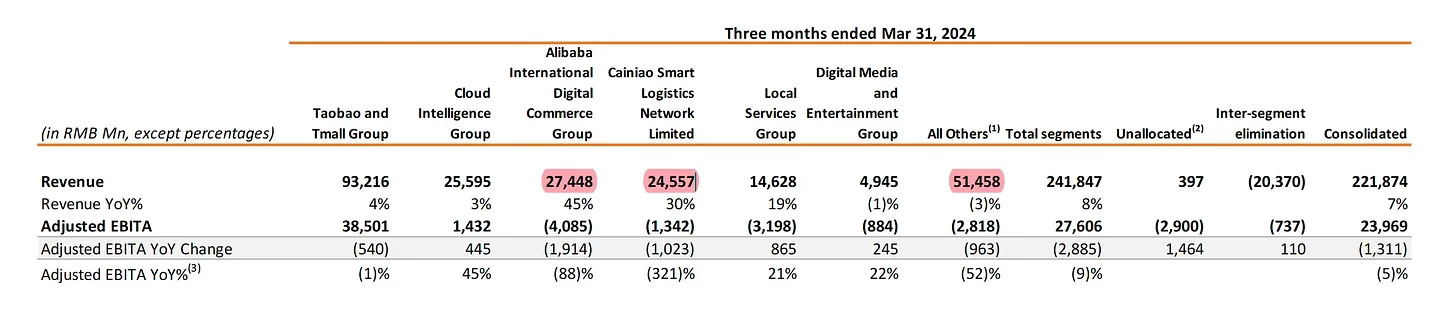

You only have to look at the “other segment” in their earnings report to see how poorly these acquisitions are performing and the mess they inherited. This “other segment” is significantly larger than international e-commerce and cloud combined.

Promising New Management

Leadership Change: New management is in place, and after some initial adjustments, they appear to have found their rhythm.

Joseph Tsai: Back in a leading position, having recently sold his stake in the Brooklyn Nets to focus more on Alibaba, he has made it clear that Alibaba will divest non-core assets. See his interview here, where he explains that he will not spend much time thinking about non-core assets.

This strategic move is expected to have several positive effects:

Removal of Underperforming Assets: Improving overall company performance.

Focused Management: Allowing management to concentrate on core strengths.

Proceeds Utilization: Using proceeds to buy back shares or invest in core areas.

Core Focus Areas

Alibaba is currently focusing on three main areas:

Chinese E-commerce

International E-commerce: Closely tied with their logistics company, Cainiao.

Local Services: Despite Ele.me being an underperforming asset, it has strategic value as instant delivery becomes increasingly important in China.

Challenges and Strategic Value

Instant Delivery: Alibaba is weaker than Meituan in this area, with Meituan’s food delivery and instant delivery business already being highly profitable. However, the strategic value of instant delivery remains significant.

Cloud Business: Faces challenges, such as government preference for Huawei and Chinese telecom companies for AI and cloud services. Additionally, due to the weak economy, Chinese companies are reluctant to invest in cloud and AI.

That provides a brief summary of the situation. If you follow Alibaba closely, this should not come as a surprise.

Back of the envelope valuation:

So, let’s not project lofty free cash flow numbers 10 years out, which is simply beyond ridiculous, especially in a highly competitive market like China. Instead, let’s conduct some very simple basic calculations.

Simple Valuation: Taking the most recent earnings from Chinese e-commerce and reducing it by 25% to account for losses in other business units.

Assumptions: Zero growth, a 10% discount rate, and an exit multiple of six.

Using these assumptions, I essentially arrive at Alibaba’s current market cap.

Of course there are

Uncertainties: Potential further losses to Pinduoduo, Douyin, and Kuaishou. Despite these uncertainties, it is not overly optimistic to assume zero growth and an exit multiple of six.

Upside Potential: The rest of the company’s businesses are essentially valued at zero, providing some upside while protecting the downside due to the cash and investments made.

I could go on about why I expect the cloud business to return to growth in the second half of 2024, and why their international e-commerce has potential. However, that’s not my aim here. I want to keep it simple and avoid discussing more details.

Conclusion

My main point is that anyone can do what I just did. By performing basic calculations, most people will arrive at almost the same result. Based on these numbers, Alibaba appears undervalued. Or let me put it this way: the downside seems protected, and there is significant upside.

So, why does this undervaluation exist, given that everyone can see it plainly?

Richard Zeckhauser wrote a beautiful article pointing out that the fear of being betrayed is one of the major causes of irrational behavior.

Being a possible sucker may be an advantage if you can gauge the probability. People are strongly averse to being betrayed. They demand much stronger odds when a betraying human rather than an indifferent nature would be the cause of a loss (Bohnet and Zeckhauser, 2004). Given that, where betrayal is a risk, potential payoffs will be too high relative to what rational decision analysis would prescribe.

This is exactly what is happening. People fear betrayal by the Chinese government or doubt the existence of the cash on the balance sheet, leading to irrational actions.

The main issue is that Alibaba stock is not included in the stock connect program. This means private investors in China cannot buy shares in Alibaba; only professional Chinese investors can do so. Most other investors are from outside China, relying on non-Chinese media.

Having more insights into China provides a tremendous edge because, in my experience, the quality of information about China in Western newspapers and about the West in Chinese newspapers is usually ridiculous. I experienced this firsthand during the COVID-19 pandemic. Newspaper coverage on both sides during the pandemic has been extremely inaccurate.

Now that I think about it, it might be a good idea to instill more fear in the market. I should rewrite this whole article and add to the fear. If we all pile on, Alibaba might be able to repurchase their shares for $50. It’s so easy to be scared when you don’t live in the country, can’t use the services, and are unfamiliar with the culture. Add to that the bad newspaper coverage, and it’s easy to distort the whole picture.

Anyways, I’m very much looking forward to August, when Alibaba is planned to have a primary listing in Hong Kong. Once this happens, their shares will be included in the Stock Connect. For reference, Chinese investors own 10% of Tencent via the Stock Connect. Let’s see how much Chinese-based investors are willing to pay for Alibaba.

I own $BABA as well and I am deeply (about -40%) in red but I‘ll let the time let play things out. I can‘t buy more as it is already a 5%+ position. I am based in Europe but I currently buy a lot of Hong Kong stocks and just bought into 0142.HK and 0882.HK You might find them interesting as well. First Pacific is rather only listed in HK but does most of its business in SEA but Tianjin is a real bargain in my opinion. It‘s a holding structure so a bit more complicated but their share in OTIS is pure gold!

I have held $BABA since 2022, and my position has been underwater since the third month of investment. Looking beyond its current e-commerce focus, Alibaba's long-term potential (5+ years) appears one of the many reasons why it faces more aggressive foreign institutional shorting compared to other Chinese ADRs.

I don't know if BABA's fundamentals need to drastically change for its stock price to go up (and remain up), because the US stock market (and the society) is extremely irrational and biased. That said, depends on the time horizon, everything will eventually revert to their intrinsic value.